Tien navigatiepunten voor goede toepassing CSRD

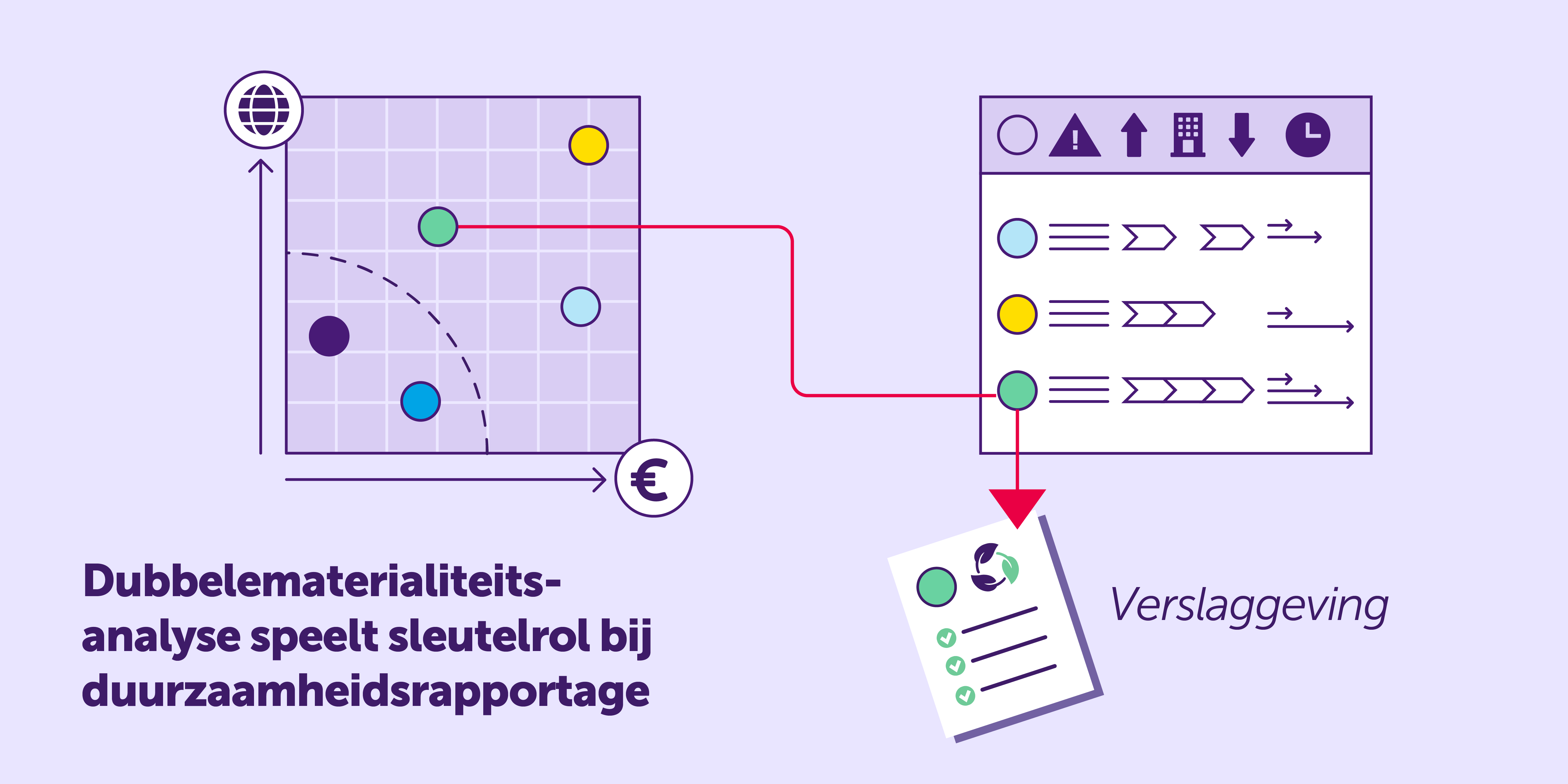

De dubbelematerialiteitsanalyse speelt een sleutelrol bij de richtlijn duurzaamheidsverslaggeving, de Corporate Sustainability Reporting Directive (CSRD). Deze geeft gebruikers van jaarverslagen inzicht in de impact, kansen en risico’s op het gebied van duurzaamheid en kan input bieden voor de strategische koers van een onderneming. Onze boodschap is duidelijk: ondanks de uitdagingen is het mogelijk om hier transparant over te rapporteren. Dit blijkt ook uit de goede voorbeelden die we nu al tegenkomen.

In het kort

• Dubbelematerialiteitsanalyse speelt sleutelrol bij CSRD; het biedt input voor duurzame en financiële koers ondernemingen

• AFM heeft gekeken naar toepassing dubbelematerialiteitsanalyse in jaarverslaggeving 2023

• 10 navigatiepunten geven ondersteuning bij opstellen dubbelematerialiteitsanalyse

• Toezicht op omgang met CSRD in jaarverslaggeving start 2024

Dubbelematerialiteitsanalyse speelt sleutelrol bij CSRD

De CSRD treedt vanaf boekjaar 2024 in werking voor grote beursgenoteerde ondernemingen. De dubbelematerialiteitsanalyse speelt daarbinnen een sleutelrol. Via deze analyse wordt duidelijk welk effect een onderneming heeft op haar omgeving (impactmaterialiteit) en hoe duurzaamheidsaspecten effect kunnen hebben op het succes van een onderneming (financiële materialiteit). Informatie is materieel wanneer het weglaten, of onjuist weergeven ervan, het oordeel van de gebruiker van de duurzaamheidsinformatie kan beïnvloeden.Hanzo van Beusekom, bestuurder AFM: 'Begrijpelijk en transparant communiceren over de dubbele materialiteit is belangrijk, omdat dit de hoeksteen is voor goede duurzaamheidsverslaggeving. In ons onderzoek zien we ook dat het kan! Het heeft 10 navigatiepunten opgeleverd waar iedereen van kan profiteren bij het maken of gebruiken van de dubbelematerialiteitsanalyse.'

Klik voor download van een Hi-res versie

Uitgeschreven tekst infographic

De infographic toont een circulair stroomschema dat gebruikers leidt van Stakeholder engagement, waar belangen en opvattingen worden opgehaald, naar Due dillegence, naar het uitwerken van de Dubbele materialiteitsanalyse tot Rapporteer, dat weer kan leiden tot nieuwe input voor gesprekken met stakeholders.

10 navigatiepunten

Stakeholder engagement: laat zien hoe stakeholders worden meegenomen1. Wees transparant over de representativiteit van stakeholder engagement.

2. Laat de ontvangen input van stakeholders zien.

Due diligence: inventariseer de duurzaamheidseffecten

3. Inventariseer duurzaamheidseffecten via due diligence.

4. Gebruik internationale handvatten, zoals OESO-richtlijnen.

5. Geef de relatie weer tussen due diligence en de dubbelematerialiteitsanalyse.

Dubbelematerialiteitsanalyse: licht analyse transparant toe

6. Maak de rol van de waardeketen inzichtelijk.

7. Koppel de bedrijfsactiviteiten aan geïdentificeerde materiële onderwerpen.

8. Geef inzicht in de materialiteitsbepaling van duurzaamheidsonderwerpen.

9. Breng de materialiteit van impact, kansen en risico's in beeld.

10. Geef de relatie weer tussen impact en risico op korte en lange termijn.

AFM heeft gekeken naar toepassing dubbelematerialiteitsanalyses in jaarverslaggeving 2023

Om inzicht te krijgen in hoe beursgenoteerde ondernemingen nu al informatie verstrekken over belangrijke thema’s in de dubbelematerialiteitsanalyses in hun jaarverslaggeving over 2023, heeft de AFM onderzoek gedaan bij 29 ondernemingen. Hieruit blijkt dat zij de nieuwe vereisten complex vinden en ze in 2023 al gestart zijn met de benodigde aanpassingen. Veel van deze bedrijven melden dat hun aanpassingsprocessen nog lopende zijn.10 navigatiepunten geven ondersteuning bij opstellen dubbelematerialiteitsanalyse

Op basis van dit onderzoek heeft de AFM 10 navigatiepunten opgesteld die ondernemingen kunnen ondersteunen bij de implementatie van de dubbelematerialiteitsanalyse in de verslaggeving. Deze zijn gebaseerd op de European Sustainability Reporting Standards (ESRS) en een aantal good practices die we nu al zien in jaarverslaggeving van beursgenoteerde ondernemingen. Hiermee kunnen gebruikers ook het gesprek met de onderneming over de koers aangaan.Toezicht op omgang met de CSRD in jaarverslaggeving 2024

In ons toezicht op de jaarverslaggeving over boekjaar 2024 beoordelen we hoe bedrijven omgaan met de CSRD. Dit doen we door middel van onze reguliere desktop-reviews. Daarnaast gaan we thematisch onderzoek doen naar een duurzaamheidsthema in verband met de naleving van de CSRD.

Contact bij dit artikel

06 31 77 76 86

Wilt u het laatste nieuws van de AFM ontvangen?

Schrijft u zich dan in voor onze nieuwsbrief, dan houden wij u op de hoogte.